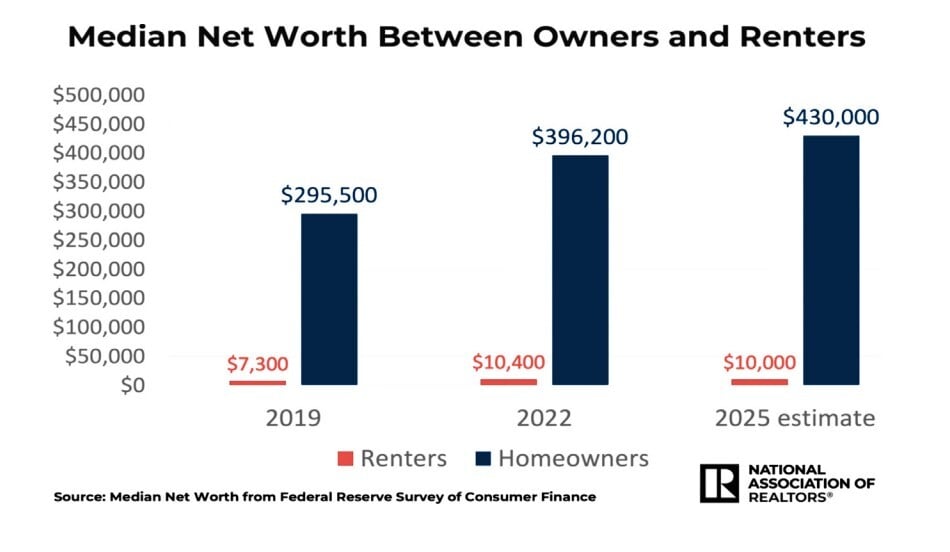

The National Association of REALTORS® recently released a sobering statistic: the average age of a first-time homebuyer in the United States is now 40 years old - an all-time high. That number matters. Not because there’s anything wrong with buying at 40 - there absolutely isn’t - but because waiting that long often means missing out on decades of wealth-building through homeownership.

... Read More